The Inflation Trap: How Sticky Prices, a Supreme Court Shock, and Gold’s $5,000 Floor Are Reshaping the Investment Landscape

WiseGold Weekly Pulse | February 27, 2026

Coverage Period: February 21, 2026 (00:00:00 EST) to February 27, 2026 (11:00:00 EST)

Executive Summary

The past week was characterized by a complex interplay of hotter-than-expected US inflation data, shifting central bank rhetoric, and significant geopolitical developments, creating a volatile but ultimately range-bound environment for most asset classes. The dominant theme was the market’s recalibration of Federal Reserve policy expectations following a surprisingly strong January Producer Price Index (PPI) report, which tempered hopes for imminent and aggressive rate cuts. This was counterbalanced by a landmark Supreme Court ruling that invalidated certain presidential tariff powers, injecting a new layer of uncertainty into trade policy. Concurrently, high-stakes US-Iran nuclear negotiations in Geneva concluded without a deal, keeping geopolitical risk premium elevated and supporting oil prices. Precious metals saw significant volatility; gold established a foothold above the psychologically important $5,000/oz level, while platinum experienced a dramatic surge. The week concluded with equity markets under pressure, weighed down by the inflation data and growing concerns over the disruptive economic impact of artificial intelligence on the software sector.

Key Takeaways:

- Hotter-than-expected US PPI data dampened expectations for near-term Federal Reserve rate cuts.

- A Supreme Court ruling on tariffs has introduced significant uncertainty into US trade policy.

- Geopolitical tensions remain elevated as US-Iran nuclear talks ended without a conclusive agreement.

- Gold consolidated above $5,000/oz, while platinum saw a significant price surge on industrial demand signals.

- Equity markets faced headwinds from inflation data and concerns over AI-driven economic disruption.

Market & Macro Week-in-Review Timeline

- Fri Feb 20: The US Supreme Court rules that the International Emergency Economic Powers Act (IEEPA) does not grant the President authority to impose tariffs, invalidating a key tool used for recent trade actions. In response, the administration announces a new temporary 10% global tariff under a different authority. [1] [2]

- Mon Feb 23: Federal Reserve Governor Christopher Waller delivers a speech on the economic outlook, noting the labor market’s surprising January strength but expressing caution, stating he needs to see February data before judging if a rebound is sustained. He characterizes the odds of a March rate cut versus a pause as a “coin flip”. [3]

- Tue Feb 24: Bank of England Governor Andrew Bailey states that a March rate cut is a “genuinely open question,” signaling a potential dovish pivot. [4] In the US, the VIX volatility index surges to its highest level in 2026 amid concerns over AI’s impact on software stocks and the new tariff regime. [5]

- Wed Feb 25: JP Morgan raises its year-end 2026 gold price forecast to $6,300/oz, citing sustained central bank demand and expected investor inflows. [6] Platinum prices surge over 5% on signs of strong industrial demand and capital rotation. [7]

- Thu Feb 26: US-Iran nuclear negotiations in Geneva conclude without a deal, though talks are expected to continue. [8] Bank of Japan Governor Kazuo Ueda signals a potential rate hike in March or April, strengthening the yen. [9] The S&P 500 and Nasdaq Composite fall as a post-earnings dip in Nvidia weighs on the tech sector. [10]

- Fri Feb 27 (10:00): The Bureau of Labor Statistics reports that the Producer Price Index (PPI) for January rose 0.5% month-over-month, with the core reading up 0.8%, both significantly exceeding economists’ expectations and signaling persistent inflationary pressures. [11]

Thematic Deep Dives

Macro & Monetary Policy

The monetary policy landscape was dominated by communications from the Federal Reserve. Governor Waller’s speech on Monday set a cautious-to-neutral tone, acknowledging the unexpectedly strong January jobs report but emphasizing the need for more data to confirm a trend after a weak 2025. His “coin flip” analogy for the March FOMC meeting encapsulated the market’s uncertainty. However, this was largely overshadowed by Friday’s hot PPI report, which significantly shifted market pricing away from an imminent rate cut. Abroad, the Bank of England appeared more dovish, while the Bank of Japan signaled a potential hawkish turn, with Governor Ueda floating a March or April rate hike for the first time.

- Fed: Remains data-dependent, with the strong January PPI print reducing the probability of a March rate cut.

- ECB: Largely quiet, with markets pricing in an extended hold.

- BoE: Governor Bailey’s comments suggest a March cut is a live possibility.

- BoJ: Governor Ueda’s remarks have increased expectations for a rate hike in the coming months.

Inflation & Growth Data

Inflation data was the primary market mover this week. The January US Producer Price Index (PPI) came in significantly hotter than anticipated, with the headline number up 2.9% year-over-year and the core up 3.6%. This data suggests that inflationary pressures are more persistent than previously thought, challenging the narrative of a smooth disinflationary path and complicating the Federal Reserve’s policy decisions. In contrast, Q4 2025 GDP growth was confirmed at a slower 1.4% annualized rate, reflecting the impact of the prior year’s government shutdown. Flash PMI data for February presented a mixed picture, with US business activity growth slowing to a 10-month low, while the Eurozone composite PMI showed surprising resilience.

- US PPI (Jan): Headline +2.9% YoY; Core +3.6% YoY, both exceeding forecasts. [11]

- US GDP (Q4 2025): Confirmed at 1.4% annualized growth, a slowdown from Q3. [12]

- US Flash PMI (Feb): Composite index fell to 52.3, indicating slowing growth in business activity. [13]

- Eurozone Flash PMI (Feb): Composite index rose to 51.9, showing unexpected improvement. [14]

Rates & Yield Curve Dynamics

US Treasury yields experienced significant volatility, initially declining on safe-haven flows before spiking sharply on Friday following the PPI release. The benchmark 10-year Treasury yield fell below 4.00% mid-week amid concerns over AI-driven economic disruption and geopolitical risk, but jumped back above this level after the inflation data. By the end of the coverage period, the 10-year yield was trading around 3.98%. The yield curve remains inverted, though the spread between the 2-year and 10-year yields fluctuated with changing Fed policy expectations. The market is now pricing a lower probability of a rate cut at the March FOMC meeting.

- 10-Year Treasury Yield: Traded in a range of approximately 3.97% to 4.05%, ending the week near the lower end of that range despite the inflation surprise. [15]

- Yield Curve: Remained inverted, reflecting market expectations of a future economic slowdown.

- Fed Funds Futures: Pricing shifted to reflect a lower likelihood of a March rate cut following the strong PPI data.

FX & Dollar Landscape

The US Dollar Index (DXY) was volatile but ended the week with a modest gain, set for its first monthly increase since October 2025. The dollar initially weakened following the Supreme Court’s tariff ruling but found support from the hot PPI data and safe-haven demand amid equity market weakness. The Euro traded in a tight range against the dollar, ending the week around 1.18. The Japanese Yen was a notable outperformer, strengthening against the dollar after the Bank of Japan governor hinted at a potential near-term rate hike, pushing USD/JPY below 156.

- DXY: Traded in a range of roughly 97.65 to 98.00, ending the week stronger. [16]

- EUR/USD: Remained largely range-bound, trading around the 1.18 level. [17]

- USD/JPY: The Yen strengthened significantly, with the pair falling from above 156 to below 155.65. [9]

Energy & Broader Commodities Context

Energy markets were primarily driven by geopolitical headlines. Crude oil prices rose, with Brent crude trading in a range of roughly $69-$73 per barrel, as the lack of a resolution in the US-Iran nuclear talks kept the market on edge. Analysts revised their 2026 oil price forecasts higher, citing the persistent geopolitical risk premium. Natural gas prices, however, continued to fall, posting a fourth straight week of losses amid milder weather forecasts and ample supply. In the broader commodity space, copper prices were firm, supported by expectations of continued demand and potential supply disruptions.

- WTI Crude Oil: Traded in a range of approximately $65-$66/bbl. [18]

- Brent Crude Oil: Traded in a range of approximately $69-$73/bbl. [19]

- Natural Gas: Prices continued to decline, with the March NYMEX contract closing near $2.86/MMBtu. [20]

Precious Metals Focus

Precious metals had a strong week, with notable moves in platinum and gold. Gold traded firmly above $5,000/oz for the entire week and pushed towards $5,240/oz, supported by ETF inflows and a dip in real yields. Silver also saw strong buying, approaching the $93/oz level. The standout performer was platinum, which surged over 5% on Wednesday to nearly $2,300/oz, driven by what appeared to be significant industrial and speculative buying. Palladium remained more subdued, trading just below $1,800/oz. Analyst forecasts for gold turned increasingly bullish, with JP Morgan issuing a $6,300/oz target for year-end 2026.

- Gold Price Range: Approximately $5,168 — $5,243/oz. [21]

- Silver Price Range: Approximately $87 — $93/oz. [21]

- Platinum Price Range: Approximately $2,170 — $2,300/oz. [7]

- Palladium Price Range: Approximately $1,765 — $1,818/oz. [22]

- Positioning: The latest Commitment of Traders (COT) report (data as of Feb 17) showed that managed funds slightly increased their net-long exposure in gold and silver, suggesting a tentative return of bullish sentiment. [23]

Credit & Liquidity

Credit markets showed early signs of strain after a period of resilience. Global credit spreads widened, with both investment-grade and high-yield bonds seeing increased risk premiums. While spreads remain near historical lows, the move suggests that concerns over persistent inflation, potential economic slowdown, and tightening liquidity are beginning to impact the corporate bond market. The focus remains on whether the robust performance of credit can continue in the face of a more cautious Federal Reserve and potential economic headwinds.

- Investment Grade Spreads: Widened slightly but remain tight by historical standards.

- High Yield Spreads: Also widened, reflecting increased risk aversion.

- Liquidity: Concerns over tightening liquidity conditions are becoming more prominent in market commentary.

Equity & Volatility Sentiment

Equity markets finished the week on the back foot, with the S&P 500 and Nasdaq Composite posting losses. The primary driver of the sell-off was a combination of the hot PPI report and mounting concerns about the disruptive impact of AI on the technology sector, particularly software companies. Nvidia’s strong earnings report was not enough to sustain a rally, and the stock sold off, dragging the broader tech sector down with it. The CBOE Volatility Index (VIX) spiked to its highest level of 2026, reflecting a significant increase in investor anxiety.

- S&P 500: Ended the week lower, on track for a monthly loss. [10]

- Nasdaq Composite: Underperformed, with significant selling pressure in software and AI-related stocks. [10]

- VIX: Surged to over 17, indicating a sharp rise in expected market volatility. [5]

Geopolitics & Strategic Risk

Geopolitical risk remains a key focus for markets. The third round of US-Iran nuclear talks in Geneva concluded without a breakthrough, ensuring that the risk of a military confrontation and its potential impact on oil supplies remains elevated. In parallel, the US Supreme Court’s decision to strike down the President’s authority to impose tariffs under the IEEPA has created a new front of strategic uncertainty. The administration’s immediate response with a new, albeit temporary, 10% global tariff highlights the ongoing potential for trade policy to be a source of market volatility.

- US-Iran Relations: Nuclear talks remain stalled, keeping geopolitical tensions high and supporting oil prices.

- US Trade Policy: The Supreme Court ruling has created significant uncertainty around tariffs, with the potential for ongoing trade disputes.

Structural & Long-Term Themes

Structural themes continue to evolve. Investment in Artificial Intelligence (AI) remains a powerful driver of capital spending, but concerns are growing about its disruptive potential, as evidenced by the sell-off in software stocks. The theme of de-dollarization and central bank diversification continues to gain traction, providing a structural tailwind for gold. In Europe, defense spending is accelerating rapidly in response to the ongoing conflict in Ukraine, with Germany, in particular, announcing significant budget increases. This trend is likely to have long-term implications for fiscal policy and industrial production in the region.

- AI Investment: Continues at a rapid pace, but market is now grappling with the negative disruptive effects alongside the productivity gains.

- De-dollarization: Central bank demand for gold remains a key structural support for the metal.

- European Defense Spending: A significant and accelerating trend with long-term fiscal and industrial implications.

Cross-Asset Interlinkages

- Hotter US PPI data led to a sell-off in US Treasuries (yields higher), a stronger US Dollar, and weakness in equities, as markets priced in a more hawkish Federal Reserve.

- Geopolitical uncertainty from the US-Iran standoff provided a risk premium for crude oil, which in turn contributed to headline inflation concerns.

- Concerns over AI-driven disruption in the tech sector led to a sell-off in software stocks, which weighed on the broader Nasdaq and S&P 500 indices and increased demand for safe-haven assets like US Treasuries.

- The strengthening of the Japanese Yen following the BoJ’s hawkish commentary created a headwind for Japanese equities but was a sign of shifting global monetary policy dynamics.

- Strong inflows into gold and silver ETFs, coupled with a dip in real yields, provided a strong tailwind for precious metals prices, allowing gold to consolidate above $5,000/oz.

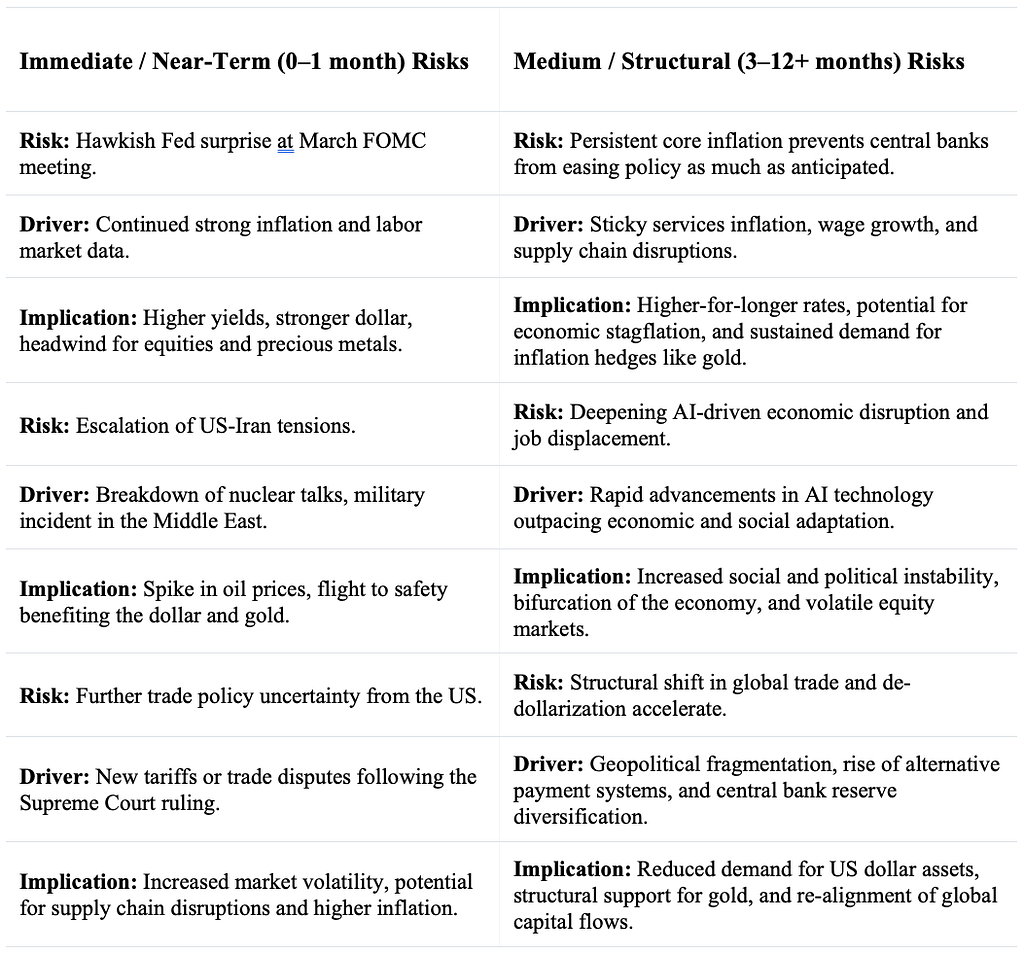

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

Event: February US Employment Report (due March 6)

- Probability: Base

- Note: A key data point for the Fed. A strong report would further reduce the odds of a March rate cut and could weigh on risk assets. A weak report would revive easing expectations. Precious metals sensitivity: A weak report would likely be bullish for gold.

Event: March FOMC Meeting (March 17–18)

- Probability: Base

- Note: The market is currently pricing a low probability of a rate cut. The focus will be on the statement, projections, and press conference for clues on the future path of policy. Hawkish surprise = potential headwind to bullion.

Event: Ongoing US-Iran Negotiations

- Probability: Elevated

- Note: Any headlines suggesting either a breakthrough or a complete breakdown of talks will have an immediate impact on oil prices and broader risk sentiment.

Portfolio Context & Implications

The developments of the past week underscore the importance of maintaining a diversified portfolio capable of navigating a complex and uncertain macroeconomic environment. The persistence of inflation, coupled with the potential for economic slowdown, highlights the challenging conditions facing investors. The strong performance of precious metals, particularly gold and platinum, in this environment serves as a reminder of their potential role as a hedge against inflation, geopolitical risk, and financial market volatility. The structural drivers supporting precious metals, including central bank demand and ongoing de-dollarization trends, appear to remain firmly in place. As such, the strategic case for holding a core position in precious metals as a form of wealth protection and portfolio diversification has been reinforced by the week’s events.

Precious Metals Strategic Thesis

Diversification Attribute

Precious metals, particularly gold, have historically exhibited a low to negative correlation with traditional financial assets like stocks and bonds. This was evident this week as equities came under pressure while gold held firm. This diversification benefit can help to reduce overall portfolio volatility and improve risk-adjusted returns over the long term.

Wealth Protection & Purchasing Power

In an environment of persistent inflation and currency debasement, precious metals can serve as a store of value and a means of preserving purchasing power. Unlike fiat currencies, which can be printed in unlimited quantities, the supply of precious metals is finite. This intrinsic scarcity provides a long-term anchor of value.

Drawdown Mitigation & Crisis Optionality

During periods of extreme market stress or geopolitical crisis, gold has often acted as a safe-haven asset, appreciating in value as other assets decline. This “crisis optionality” can help to mitigate portfolio drawdowns and provide liquidity when it is needed most. The elevated geopolitical risk premium currently supporting gold is a clear example of this dynamic.

Structural Demand Drivers

Beyond their monetary characteristics, precious metals benefit from diverse and growing sources of demand. This includes industrial applications for silver and platinum group metals in areas like solar energy and automotive catalysts, as well as consumer demand for gold jewelry. Crucially, the ongoing trend of central bank diversification away from the US dollar and into gold provides a strong and sustained source of demand.

Allocation Framing

A strategic allocation to precious metals can be viewed as a form of portfolio insurance. While the specific allocation will depend on an individual’s risk tolerance and financial goals, historical analysis suggests that a modest allocation to gold and other precious metals can enhance portfolio resilience across a range of economic scenarios. This is not a tactical trade but a long-term strategic holding.

Summary Capsule

- Macro Pulse: US inflation proves sticky, pushing back Fed rate cut expectations and increasing stagflation concerns.

- Metals Stance: Gold solidifies its position above $5,000/oz, with platinum showing significant strength, reinforcing the bullish thesis for precious metals.

- Risk Tone: Geopolitical and trade policy uncertainty remain elevated, providing a supportive backdrop for safe-haven assets.

- Positioning Nuance: Tentative signs of renewed bullish positioning in precious metals futures, though conviction is not yet strong.

- Forward Watch: The February US jobs report and the March FOMC meeting are the next key catalysts for the market.

- Structural Theme: The dual forces of AI disruption and de-dollarization continue to shape the long-term investment landscape.

Source List

[1] PIIE — What the Supreme Court’s tariff ruling changes, and what it doesn’t — February 20, 2026 — https://www.piie.com/blogs/realtime-economics/2026/what-supreme-courts-tariff-ruling-changes-and-what-it-doesnt [2] White House — Fact Sheet: President Donald J. Trump Imposes a Temporary Import Duty to Address Fundamental International Payment Problems — February 20, 2026 — https://www.whitehouse.gov/fact-sheets/2026/02/fact-sheet-president-donald-j-trump-imposes-a-temporary-import-duty-to-address-fundamental-international-payment-problems/ [3] Federal Reserve — Speech by Governor Waller on the economic outlook — February 23, 2026 — https://www.federalreserve.gov/newsevents/speech/waller20260223a.htm [4] Reuters — Bank of England’s Bailey says March rate cut is ‘genuinely open question’ — February 24, 2026 — https://www.reuters.com/world/uk/bank-englands-bailey-says-march-rate-cut-is-genuinely-open-question-2026-02-24/ [5] Financial Content — VIX Hits 2026 Peak as ‘Software-mageddon’ and New Tariffs Rattle Markets — February 24, 2026 — http://markets.financialcontent.com/stocks/article/marketminute-2026-2-24-fear-returns-to-wall-street-vix-hits-2026-peak-as-software-mageddon-and-new-tariffs-rattle-markets [6] Reuters — JP Morgan expects gold prices to reach $6300/oz by end-2026 — February 25, 2026 — https://www.reuters.com/business/finance/jp-morgan-expects-gold-prices-reach-6300oz-by-end-2026-2026-02-25/ [7] Texas Precious Metals — Precious Metals Market Update: Platinum Surges 5.6% as Silver Nears $90 — February 25, 2026 — https://texmetals.com/all-news/precious-metals-market-update-2-25-2026 [8] Al Jazeera — US-Iran talks conclude with claims of progress but few details — February 26, 2026 — https://www.aljazeera.com/news/2026/2/26/us-iran-talks-conclude-claims-progress-few-details [9] Reuters — BOJ chief flags March, April rate-hike chance in Yomiuri interview — February 25, 2026 — https://www.reuters.com/world/asia-pacific/boj-chief-says-bank-will-scrutinise-data-march-april-meetings-yomiuri-reports-2026-02-25/ [10] Investopedia — Markets News, Feb. 26, 2026: S&P 500, Nasdaq Drop After 2 Days of Gains — February 26, 2026 — https://www.investopedia.com/stock-market-today-dow-jones-s-and-p-500-02262026-11914836 [11] CNBC — Core wholesale prices rose 0.8% in January, much more than expected — February 27, 2026 — https://www.cnbc.com/2026/02/27/ppi-january-2026-.html [12] The Guardian — US economic growth slowed in fourth quarter of 2025 amid government shutdown — February 20, 2026 — https://www.theguardian.com/business/2026/feb/20/economic-growth-fourth-quarter-2025 [13] S&P Global — Flash US PMI — February 20, 2026 — https://www.pmi.spglobal.com/Public/Home/PressRelease/de7251a734954460986e49e0ab041b2f [14] WHBL — Euro zone businesses perform better than expected in February, PMI shows — February 20, 2026 — https://whbl.com/2026/02/20/euro-zone-business-activity-improved-in-february-as-manufacturing-bounced-back-pmi-shows/ [15] CNBC — U.S. Treasury yields: investors react to hot wholesale inflation — February 27, 2026 — https://www.cnbc.com/2026/02/27/us-treasury-yields-investors-await-wholesale-inflation-reading.html [16] Mitrade — US Dollar Index (DXY) eases despite stronger-than-expected US PPI — February 27, 2026 — https://www.mitrade.com/au/insights/news/live-news/article-4-1511049-20260227 [17] Forex.com — EUR/USD Analysis: The euro approaches the end of the week with a consistent neutral bias — February 26, 2026 — https://www.forex.com/en-us/news-and-analysis/eurusd-analysis-the-euro-approaches-the-end-of-the-week-with-a-consistent-neutral-bias/ [18] MarketWatch — Crude Oil Apr 2026 Overview — CLJ26 — February 27, 2026 — https://www.marketwatch.com/investing/future/clj26 [19] Rigzone — Oil Market Is Nervous for the Coming Weekend — February 27, 2026 — https://www.rigzone.com/news/oil_market_is_nervous_for_the_coming_weekend-27-feb-2026-183087-article/ [20] Sprague Energy — Natural Gas Analysis: Price Changes and Forecasts — February 27, 2026 — https://www.spragueenergy.com/natural-gas-analysis-price-changes-and-forecasts/ [21] BullionVault — Gold Sets 1st Full Week Above $5000 as Silver’s Giant SLV ETF Also Grows — February 27, 2026 — https://www.bullionvault.com/gold-news/gold-price-news/gold-5000-week-silver-etf-022720261 [22] Trading Economics — Palladium — Price — Chart — Historical Data — News — February 27, 2026 — https://tradingeconomics.com/commodity/palladium [23] StoneX — Commodity Futures Positioning: Metals & Oil | COT Report — 23 Feb 2026 — February 23, 2026 — https://www.stonex.com/en/market-intelligence/commodity-futures-positioning-metals-oil-cot-report-23-feb-2026/

Methodology & Notes

Data is compiled from credible public sources, including financial news outlets, government statistical agencies, and central bank publications. Price ranges are approximated based on available spot and front-month futures data within the coverage window. All timestamps are EST. The report aims to include key data releases up to 10:00 AM EST on the date of publication.

Disclosure

This report is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #Gold #PreciousMetals #MacroOutlook #FixedIncome #FederalReserve #Inflation #WealthManagement #AlternativeAssets #Geopolitics #PortfolioStrategy #CommodityMarkets #HardAssets #Platinum #Silver #GlobalMacro